传感器是一种检测装置,能感受到被测量的信息,并能将感受到的信息,按一定规律变换成为电信号或其他所需形式的信息输出,以满足信息的传输、处理、存储、显示、记录和控制等要求。

根据传感器的基本感知功能可分为热敏元件、光敏元件、气敏元件、力敏元件、磁敏 元件、湿敏元件、声敏元件、放射线敏感元件、色敏元件和味敏元件等十大类。这些可 以归为物理类,化学类,生物类三大块。

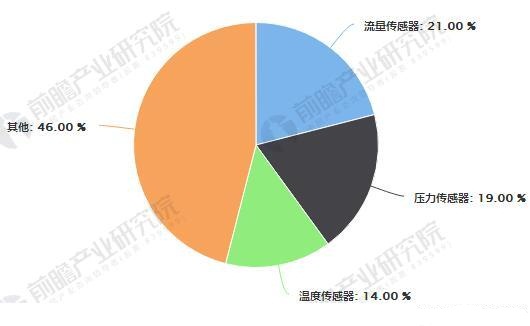

从传感器种类来看,流量传感器、压力传感器、温度传感器占据最大的市场份额,分别占21%、19%、14%。从应用领域来看,工业、汽车电子、通信电子、消费电子四部分是传感器最大的市场。国内工业和汽车电子产品领域的传感器占比约42%左右,而发展最快的是汽车电子和通信电子应用市场。

传感器市场规模持续快速增长

据前瞻产业研究院发布的《传感器制造行业发展前景与投资预测分析报告》统计数据显示,近年来,我国传感器市场持续快速增长,年均增长速度超过20%,2011年中国传感器市场规模为480亿元,到了2016年中国传感器市场规模突破千亿元,达到1126亿元。到2017年中国传感器市场规模增至1300亿元,同比增长15.45%。

中国传感器企业布局分析

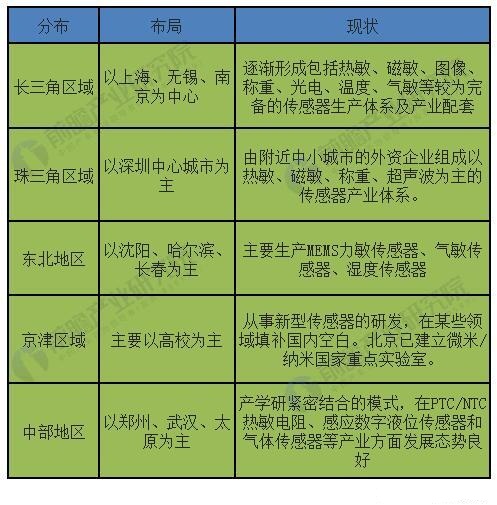

目前我国传感器企业正努力追赶国外企业,并出现区域的传感器企业集群,企业主要集中在长三角地区,并逐渐形成以北京、上海、南京、深圳、沈阳和西安等中心城市为主的区域空间布局。其中,主要传感器企业有接近一半的比例分布在长三角地区,其他依次为珠三角、京津地区、中部地区及东北地区等。

中国传感器企业布局情况

近年来,传感器技术发展与创新的重点在材料、结构和性能改进3个方面:敏感材料从液态向半固态、固态方向发展;结构向小型化、集成化、模块化、智能化方向发展;性能向检测量程宽、检测精度高、抗干扰能力强、性能稳定、寿命长久方向发展。随着物联网技术的发展,对传统传感技术又提出了新的要求,产品正逐渐向微机电系统(MEMS)技术(如:纳米技术、薄膜技术)、无线数据传输技术、新材料技术、复合传感器技术、结合数模处理器等多学科交叉融合的方向发展。

目前,传感器的五大主要应用领域为工业、医疗、汽车电子、通信电子、消费电子。其中,在国内,工业和汽车电子用传感器占比较大,发展最快的是汽车电子和通信电子应用市场。此外,环境监测、油气管道、智能电网、可穿戴设备等领域的创新应用将成为新热点,有望在未来创造更多的市场需求。

传感器作为物联网的心脏,发展空间巨大。物联网的系统架构一般由感知层、传输层和应用层组成,其中,感知层主要由传感器、微处理器和无线通信收发器等组成。预计到2025年物联网带来的经济效益将在2.7万亿到6.2万亿美元之间。其中,传感器作为数据采集的入口、物联网的“心脏”,将迎来巨大的发展空间。

同时由于目前国内智能传感器国外品牌占据绝大部分市场份额,国内进口产品的替代空间非常大,随着本土企业加快研发进程和智能传感器产业链布局,中国智能传感器市场未来将保持较快的发展速度,本土化率将不断提高。(转自前瞻网)

Sensor is a kind of detection device, which can sense the measured information and transform the sensed information into electrical signals or other required forms of information output according to certain rules to meet the requirements of information transmission, processing, storage, display, recording and control.

According to the basic sensing function of the sensor, it can be divided into ten categories: thermal sensor, photosensor, gas sensor, force sensor, magnetic sensor, humidity sensor, sound sensor, radiation sensor, color sensor and taste sensor. These can be classified into three parts: Physics, chemistry and biology.

According to the types of sensors, flow sensors, pressure sensors and temperature sensors occupy the largest market share, accounting for 21%, 19% and 14% respectively. From the perspective of application field, industry, automotive electronics, communication electronics, consumer electronics are the largest sensor market. About 42% of the sensors in the field of industrial and automotive electronics products in China, and the fastest growing market is automotive electronics and communication electronics.

The scale of sensor market continues to grow rapidly.

According to the statistics released by the Institute of Prospective Industry, the sensor manufacturing industry development prospects and investment forecast analysis report shows that in recent years, China's sensor market has been growing rapidly, with an average annual growth rate of more than 20%. In 2011, China's sensor market size was 48 billion yuan, and in 2016, China's sensor market size broke through. 100 billion yuan, reaching 112 billion 600 million yuan. By 2017, the scale of China's sensor market increased to 130 billion yuan, an increase of 15.45% over the same period last year.

Layout analysis of sensor enterprises in China

At present, China's sensor enterprises are trying to catch up with foreign enterprises, and there is a regional sensor enterprise cluster. The enterprises are mainly concentrated in the Yangtze River Delta region, and gradually form a regional spatial layout with Beijing, Shanghai, Nanjing, Shenzhen, Shenyang and Xi'an as the main cities. Among them, nearly half of the major sensor enterprises are distributed in the Yangtze River Delta region, and the others are the Pearl River Delta, Beijing-Tianjin region, central region and northeast region in turn.

Layout of sensor enterprises in China

In recent years, the development and innovation of sensor technology focus on three aspects: material, structure and performance improvement: sensitive materials from liquid to semi-solid, solid-state direction; structure to miniaturization, integration, modularization, intelligent direction; performance to wide detection range, high detection accuracy, strong anti-interference ability, stable performance. Long service life. With the development of the Internet of Things technology, new requirements have been put forward for the traditional sensing technology. The products are gradually developing towards the multi-disciplinary integration of micro-electro-mechanical system (MEMS) technology (such as nano-technology, thin film technology), wireless data transmission technology, new material technology, composite sensor technology, combined with digital-analog processor and so on.

At present, the five main application fields of sensors are industry, medical, automotive electronics, communication electronics, consumer electronics. Among them, industrial and automotive electronic sensors account for a larger proportion in China, the fastest growing is the automotive electronic and communication electronic application market. In addition, innovative applications in environmental monitoring, oil and gas pipelines, smart grids, wearable equipment and other fields will become new hot spots, and it is expected to create more market demand in the future.

As the heart of the Internet of things, sensors have huge room for development. The system architecture of the Internet of Things is generally composed of perception layer, transmission layer and application layer. The perception layer is mainly composed of sensors, microprocessors and wireless communication transceivers. It is estimated that the economic benefits of the Internet of things will be between 2 trillion and 700 billion and 6 trillion and 200 billion dollars by 2025. Among them, sensors as the entrance of data acquisition, the "heart" of the Internet of Things, will usher in a huge space for development.

At the same time, due to the current domestic smart sensor foreign brands occupy the majority of the market share, the domestic imported products have a very large space for substitution. With the accelerated development process of local enterprises and smart sensor industry chain layout, China's smart sensor market will maintain a relatively rapid development rate in the future, the localization rate will continue to increase.